All Categories

Featured

Table of Contents

The are entire life insurance policy and global life insurance policy. grows cash money value at a guaranteed rate of interest and additionally through non-guaranteed dividends. grows cash value at a fixed or variable rate, depending upon the insurance firm and plan terms. The money value is not contributed to the death benefit. Cash money worth is a function you capitalize on while to life.

The policy car loan rate of interest rate is 6%. Going this route, the rate of interest he pays goes back right into his plan's money worth rather of an economic institution.

Dbs Bank Visa Infinite Debit Card

Nash was a money professional and fan of the Austrian school of economics, which advocates that the worth of items aren't clearly the result of typical economic frameworks like supply and need. Rather, people value cash and products in a different way based on their economic standing and needs.

One of the mistakes of conventional banking, according to Nash, was high-interest rates on lendings. Way too many people, himself included, obtained right into economic difficulty due to reliance on banking institutions. So long as financial institutions set the rates of interest and funding terms, people didn't have control over their very own wide range. Becoming your very own lender, Nash figured out, would certainly place you in control over your financial future.

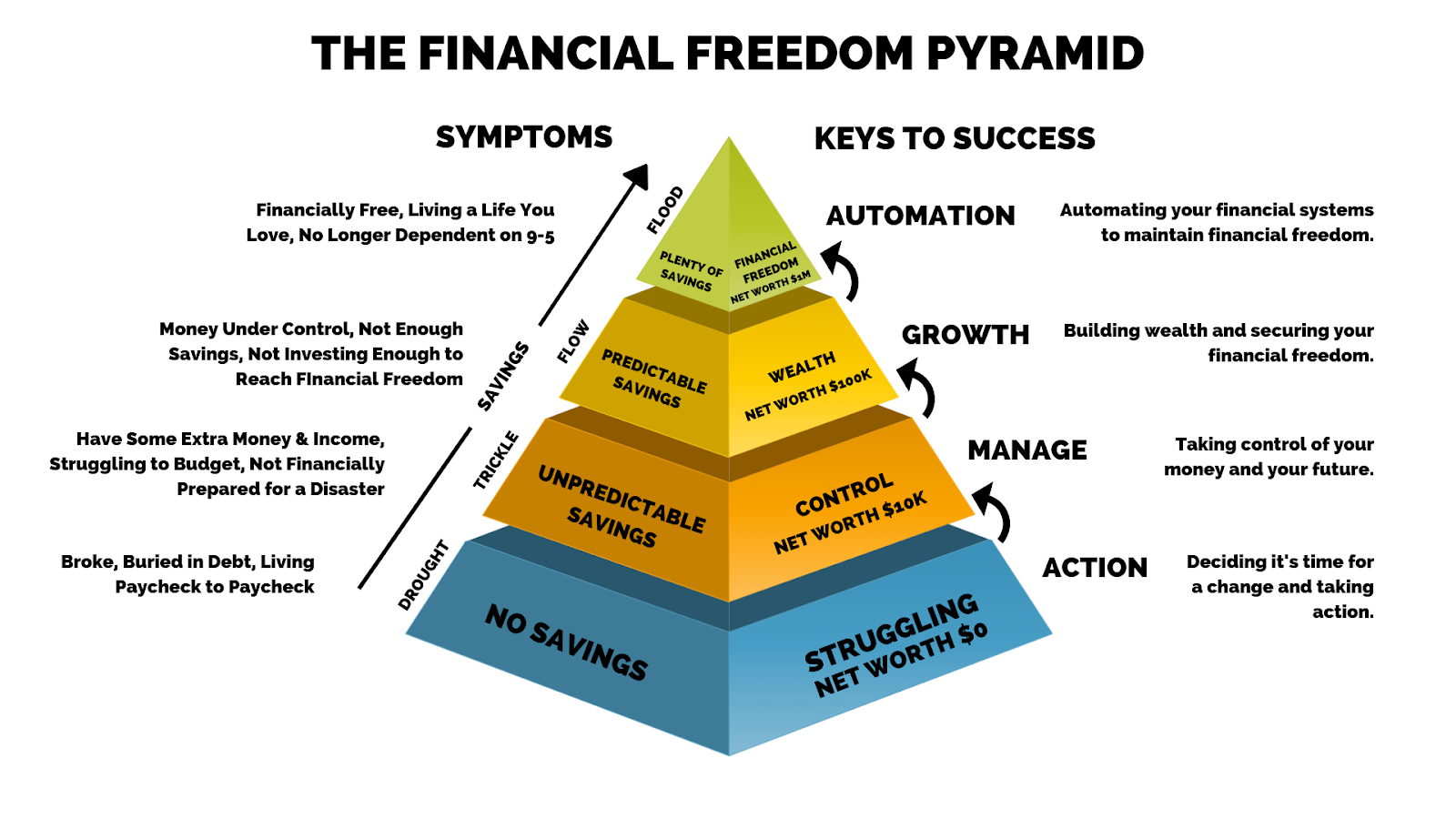

Infinite Banking needs you to possess your monetary future. For ambitious people, it can be the ideal financial device ever before. Right here are the advantages of Infinite Financial: Perhaps the solitary most advantageous aspect of Infinite Financial is that it boosts your money circulation.

Dividend-paying entire life insurance policy is very reduced danger and offers you, the policyholder, a terrific deal of control. The control that Infinite Banking uses can best be organized right into 2 categories: tax advantages and asset defenses - my wallet be your own bank. Among the reasons whole life insurance coverage is optimal for Infinite Financial is how it's strained.

Infinite Banking Concept Book

When you use entire life insurance coverage for Infinite Banking, you enter into an exclusive agreement between you and your insurance coverage business. These securities may vary from state to state, they can consist of protection from possession searches and seizures, protection from reasonings and defense from lenders.

Entire life insurance coverage policies are non-correlated properties. This is why they work so well as the financial structure of Infinite Banking. No matter of what happens in the marketplace (stock, property, or otherwise), your insurance coverage keeps its well worth. Way too many individuals are missing this vital volatility barrier that aids safeguard and grow wide range, rather splitting their money into 2 pails: savings account and investments.

Entire life insurance coverage is that 3rd bucket. Not only is the price of return on your whole life insurance policy assured, your fatality advantage and premiums are additionally ensured.

Below are its major advantages: Liquidity and ease of access: Policy finances supply prompt accessibility to funds without the restrictions of conventional bank lendings. Tax efficiency: The cash money value expands tax-deferred, and plan car loans are tax-free, making it a tax-efficient tool for developing wealth.

Bank On Yourself Program

Possession security: In lots of states, the cash money worth of life insurance policy is shielded from creditors, adding an extra layer of monetary safety. While Infinite Financial has its merits, it isn't a one-size-fits-all solution, and it features substantial disadvantages. Here's why it may not be the best strategy: Infinite Financial commonly needs detailed policy structuring, which can puzzle insurance policy holders.

Picture never needing to stress over financial institution fundings or high rate of interest once again. What happens if you could obtain money on your terms and develop wealth concurrently? That's the power of limitless banking life insurance policy. By leveraging the money value of whole life insurance policy IUL policies, you can expand your wide range and borrow money without relying upon conventional banks.

There's no set lending term, and you have the freedom to select the settlement schedule, which can be as leisurely as paying off the car loan at the time of fatality. This flexibility extends to the servicing of the finances, where you can select interest-only settlements, maintaining the car loan equilibrium flat and convenient.

Holding money in an IUL repaired account being attributed interest can frequently be far better than holding the cash on down payment at a bank.: You have actually constantly desired for opening your own bakery. You can borrow from your IUL plan to cover the first expenses of renting out a space, buying tools, and employing staff.

Infinite Banking Wiki

Individual financings can be gotten from conventional financial institutions and credit unions. Below are some key points to take into consideration. Charge card can provide a versatile way to obtain money for very short-term durations. However, borrowing money on a charge card is normally really pricey with interest rate of interest (APR) often reaching 20% to 30% or even more a year.

The tax obligation therapy of plan finances can differ substantially relying on your nation of home and the specific terms of your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan lendings are typically tax-free, supplying a considerable advantage. In various other territories, there may be tax obligation implications to take into consideration, such as prospective tax obligations on the lending.

Term life insurance policy just offers a survivor benefit, with no cash worth buildup. This implies there's no cash worth to borrow versus. This write-up is authored by Carlton Crabbe, President of Capital for Life, a professional in giving indexed global life insurance policy accounts. The details supplied in this article is for instructional and informational purposes only and ought to not be construed as monetary or financial investment suggestions.

Nonetheless, for funding policemans, the substantial laws enforced by the CFPB can be viewed as cumbersome and limiting. Initially, loan policemans frequently say that the CFPB's regulations produce unnecessary bureaucracy, bring about even more documents and slower loan processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) rule and the Ability-to-Repay (ATR) demands, while targeted at protecting customers, can result in hold-ups in closing bargains and increased operational prices.

{kind=link}

Latest Posts

Bank On Yourself Problems

Bank On Yourself Review Feedback

Start Your Own Personal Bank